OMAHA, NE / ACCESS Newswire / June 10, 2025 / Some artists perform. Others uplift. But when DREION takes the stage, he transforms it. The Omaha-born singer, songwriter and foster care advocate will headline the first of three free Music at Miller Park concerts in Omaha, Nebraska on Saturday, June 28.

But this isn’t just any show for DREION. It’s a homecoming. And it’s deeply personal.

DREION’s love for music began in the pews of Grace Apostolic Worldwide Ministries. That early spark, nurtured by family musicians and Omaha Northwest High School educators, was further honed at Berklee College of Music and has since evolved into a bold, genre-defying sound he calls “inspirational soul and R&B.”

Last fall, DREION competed on “The Voice,” turning all four chairs with his soulful rendition of “Shining Star” by Earth, Wind & Fire. But his story didn’t start with celebrity judges – it starts with something much harder to talk about.

At seven years old, DREION entered the foster care system, enduring five placements, seven medications and repeated emotional trauma in just six months.

“I didn’t realize my story could help others until I started sharing it,” he said.

He decided to heal and tell his story through music and contacted foster care advocacy organizations to see how it could help. That led him to become a national ambassador for Earth, Wind & Fire’s Music is Unity Foundation.

“When I did that first event, I realized so many people have similar stories, and some are still experiencing it. I returned to my mother with a positive outcome, but many didn’t have a positive outcome. I knew at that moment I had to be the voice because few people share their stories. They were too scared to share their story. They were ashamed. They may not even be able to share or know how. They were too traumatized.”

His song about his experience, “Let It Rain,” was featured in the movie “Foster Boy,” which premiered in 2020. “They were finished with the movie. They loved my music so much they went back and re-edited the movie to add it in there,” he shared. “Foster Boy” is currently streaming on Peacock and Tubi.

DREION continues to be a catalyst for foster youth who can’t speak out for themselves.

He’ll be opening for Earth, Wind & Fire again this summer, including a stop at The Astro in July. During that show, DREION will welcome some foster youth from the community backstage for a behind-the-scenes experience.

“It’s one thing to tell kids their dreams are valid. It’s another thing to invite them in and show them it’s possible,” he said.

Technically, this isn’t DREION’s first Music at Miller Park concert, but it might as well be. When he was slated to perform in 2023, storms rolled in and washed the concert out after just two songs.

“I never really got to give the full show I had planned,” he said. “This is my redemption moment. And I’m pulling out all the stops.”

That includes surprise guests and interactive moments that promise to make the evening unforgettable. The crowd will also be among the first to hear his new single, “Thank You for Loving Me,” part of a larger album and tour in the works for 2026.

While his experience on “The Voice” has helped usher in numerous exciting opportunities and fame, he makes sure people know where it all started for him.

“I told them, ‘Do not say I live in Boston. I want you to say I’m from Omaha, Nebraska.’ Because it’s true and important, a lot of gifted talent has come from our city. Being a voice for that on a national level is an honor. But it’s even more of an honor when you can come back and people recognize what you’re doing and are proud of you,” he shared.

With a fresh single out, a full-length album and several exciting shows on the horizon, DREION is stepping into his moment and inviting us along for his journey.

“It’s a great opportunity to be able to come back, see people that have been supporting me, welcome people that may not know who I am, but are proud that I am from the same city that they are and want to support me, and then also be a difference maker in the community here, even though I’m not necessarily based here,” he shared.

He also looks forward to the opportunities his growing platform could bring to Omaha and foster care youth.

Music at Miller Park is free and family-friendly. The lawn opens at 5 p.m. with DREION’s performance starting at 7:30 p.m. on Saturday, June 28. To learn more, visit o-pa.org/mamp.

Toronto, Canada – June 10, 2025 –TradeCafe, a global marketplace transforming how the global spot market for physical agri-commodities transacts, today announced the appointment of Huey Lin to its Board of Directors. Lin brings rare expertise at the intersection of global logistics and fintech from leadership roles at Flexport, Affirm, and PayPal.

The appointment comes at a pivotal moment for TradeCafe as the company accelerates its mission to digitize the traditionally opaque and fragmented agri-commodity trading ecosystem. With global food security and supply chain resilience becoming increasingly critical, TradeCafe’s platform addresses fundamental inefficiencies in how agricultural products move from producers to consumers worldwide. The company’s technology-enabled approach is particularly vital as climate volatility and geopolitical tensions continue to impact global food supply chains, creating unprecedented demand for transparent, efficient trading solutions.

Adding Lin to the board strengthens TradeCafe’s board as the company expands its digital footprint and advances toward its next rounds of funding. Lin currently serves on the boards of the Singapore Exchange (SGX), Hang Seng Bank, and fintech unicorn Nium, bringing deep governance experience from both established institutions and high-growth technology companies. Her multi-market perspective spans Asia-Pacific and North American markets, providing invaluable insights for TradeCafe’s global expansion strategy.

Lin’s appointment brings critical operational expertise from the intersection of global logistics and fintech. As President of Flexport Asia she scaled the company’s most strategic and fastest-growing region and helped build technology-enabled supply chain solutions that revolutionized freight forwarding. At Affirm, she pioneered new financial products as a founding executive and COO, contributing to the company’s transformation of consumer lending. Her foundation in payments innovation began at PayPal, where she was one of the first product managers driving international expansion during the company’s formative years. Currently, Lin is an active angel investor and advisor to companies ranging from pre-seed to high-growth stages, with a particular focus on supply chain innovation and financial infrastructure.

“We’re thrilled to welcome Huey to the TradeCafe board,” said Nicholas Walker, CEO of Bassett & Walker Inc., and Director of TradeCafe. “Her rare blend of operational depth and strategic foresight, from scaling cross-border operations at Flexport to driving transparency at PayPal and Affirm, aligns perfectly with our mission to transform the global protein trade. Her insights will be instrumental as we expand our digital marketplace.”

“TradeCafe is revolutionizing how physical agri-commodities are traded in spot markets the way PayPal transformed payments,” said Lin. “I’m excited to help build infrastructure that makes global agri-commodity trading more efficient, transparent, and accessible for everyone.“

Lin’s appointment signals TradeCafe’s ambition to become the de facto clearinghouse for the $2 trillion global spot transaction market for physical agri-commodities, using technology to provide the transparency and efficiency currently missing in this industry.

About TradeCafe

TradeCafe is a forward thinking technology-driven global marketplace where buyers and sellers in the global spot transaction market for physical agri-commodities execute, finance, and fulfill transactions seamlessly. Having facilitated over $3 billion in transactions to date across more than 80 markets, TradeCafe is rapidly becoming the trusted infrastructure for spot agri-commodity trading. The platform’s comprehensive suite of tools includes price discovery, transaction management, and end-to-end fulfillment and logistics capabilities. Learn more at www.tradecafe.com.

Media Contact:

John Dietrich

Head of Marketing

TradeCafe jdietrich@tradecafe.com

+1 647-278-9269

C-level executive at Afinia provides extensive context on AstroNova’s quality issues, go-to-market failures, and MTEX technology’s reliability challenges and risks

Askeladden Capital believes AstroNova’s Board violated its fiduciary duty by acquiring MTEX with insufficient due diligence and incomplete integration plan

We believe AstroNova’s governance is careening from bad to worse, with a risky plan to build many AstroNova products on a technology base with known quality concerns – products which now also apparently face competition from MTEX’s Chinese development partner

Q1 FY26 results demonstrate AstroNova continues to underperform

Askeladden to host an open Town Hall forum for all interested parties on Thursday, June 12, at 11 AM ET

FORT WORTH, TX / ACCESS Newswire / June 10, 2025 / Dear AstroNova Shareholders,

As AstroNova’s largest shareholder, jointly with my firm Askeladden Capital (collectively, “we,”) I recently filed a definitive proxy statement soliciting your vote for five new directors at this year’s Annual Meeting on July 9 th . We will host a Town Hall via Zoom at 11:00 AM Eastern Time (10:00 AM Central Time) on Thursday, June 12, 2025, for all interested stakeholders to interact directly with our slate; we invite your toughest questions. You can register here .

Recently, we published our detailed plan for improving AstroNova’s performance, backed by extensive primary research . We believe thorough due diligence is a fiduciary duty of any Board, so we have spent the past few months interviewing relevant industry experts. We continue to extend our research; we have recently spoken to additional former high-level AstroNova employees and managers at several competitors.

Today, we release critical findings shedding further light on why the MTEX acquisition represents a severe, fundamental, and ongoing failure of governance by AstroNova’s Board, creating a compelling case for change. MTEX’s ‘disruptive’ technology – which AstroNova dramatically overpaid for, in light of the subsequent goodwill impairment – was seemingly co-developed in conjunction with a Chinese supplier, UP Group (UPG), based on printheads that UPG apparently sourced on the open market rather than directly from HP.

If that is the case, it could mean that MTEX lacked HP’s support in key technical areas potentially critical for product reliability, which could provide insight into MTEX’s reliability challenges discussed below. According to both a C-level industry executive and information on UPG’s website, UPG now seemingly competes directly against AstroNova, offering a product that appears substantially similar to AstroNova’s recently-launched QL-435.

These findings reinforce our belief that a boardroom reset is urgently needed. AstroNova’s Q1 results fail to demonstrate meaningful inflection in the business – and Mr. Woods, with the backing of the Board, continues to double down on what we believe is a deeply flawed strategy.

We cover the following topics in this letter:

Section 1 summarizes relevant MTEX history and associated governance failures.

Section 2 provides extensive further detail about key MTEX-related challenges.

Section 3 builds on our previous primary research, providing further context on numerous strategic failures by AstroNova, ranging from channel partner relationships to ink quality issues.

Section 4 briefly addresses several key lowlights from Q1 FY26 results.

In the near future, we plan to publish our comprehensive presentation, “Building a Better AstroNova,” which will summarize and visualize all of Askeladden’s published analysis, and comprehensively demonstrate how our slate of talented and motivated nominees better serves AstroNova’s shareholders at this critical juncture.

Section 1: Summary of MTEX History and Governance Failures

We recently interviewed a C-level executive at Afinia who shared many alarming insights that reflect extremely poorly on AstroNova’s governance of the MTEX acquisition from start to finish . [1] Afinia is an AstroNova competitor that seems well-regarded in the industry; a former Senior Vice President at printhead-technology vendor Memjet told us that Afinia seemed to be outcompeting AstroNova in the marketplace, despite being a smaller company with fewer resources.[2][3]

Afinia spent over a year working with MTEX to commercialize and sell an MTEX product, ultimately walking away due to serious concerns about MTEX’s technological reliability and organizational immaturity. The executive also cited specific quality concerns that could arise from the use of “multi-sourced inks” – noting that original equipment manufacturers (OEMs) such as HP, Canon, and Epson spend millions of dollars to test their ink and ensure it is optimized for the machine, and multi-sourced inks that have not undergone such testing – particularly once mixed together in the machine in unpredictable ways – could damage printheads.

AstroNova is no stranger to quality issues, nor has it proven adept at resolving them. While the Memjet ink quality issue affected many customers, the Afinia executive noted his company resolved the issue in about six months – whereas AstroNova struggled with it for over two years, which its Form 10-K discloses ultimately damaged its brand.[4] Another former AstroNova employee (on the aerospace side) expressed severe concerns about AstroNova’s quality culture, and we recently spoke to a TrojanLabel customer who has faced consistent and “existential” issues with his TrojanLabel printer and AstroNova-supplied media.[5]

With that already-tenuous backdrop, we believe that a rushed rollout of products based on immature and unreliable MTEX technology could critically and permanently damage AstroNova’s brand image.

We believe the company’s current strategy not only risks perpetuating years of underperformance, but may also jeopardize its future. Despite management’s claims that MTEX’s technology is “disruptive,” it has failed to achieve any meaningful product-market fit – prompting a basic but critical question: if MTEX’s platform truly offers transformative value, why aren’t customers buying it? Why has MTEX technology not found product-market fit?

Since the acquisition, MTEX has generated less than half of the expected revenue run-rate; in fact, sales actually declined sequentially from Q3 FY25 to Q4 FY25, and again from Q4 FY25 to Q1 FY26.[6] Compounding AstroNova’s challenges in commercializing this technology, UPG seemingly offers the same products at a lower cost; we identified a product on UPG’s website that appears identical to AstroNova’s recently launched QL-435.

Below, we present a summary of our understanding of critical MTEX-related matters leading up to the present day. We then summarize key governance failings, and share detailed insights from our interview with the Afinia executive.

MTEX historically used Memjet technology, then decided to seek alternatives.[7]

MTEX already had a reputation in the market for being unfocused and immature[8], attempting to develop too many products[9], with those products that they did develop often facing reliability issues.[10] (The Afinia executive: “ Everyone in the industry knew [the Atom 1] didn’t work.” )[11]

MTEX partnered with a Chinese supplier[12], UPG[13], to develop new products based on HP printheads; a former AstroNova sales leader called these specific printheads “ basically very cheap. It’s more of a desktop-style printhead from HP.” [14] However, these HP printheads were apparently not sourced directly from HP – and HP did not participate directly in the development process of the products. [15]

This development process lacked critical input from the printhead manufacturer, including component optimization, software, and expertise in building and servicing “maintenance modules” – all of which might lead to printhead damage and maintenance challenges. [16]

An MTEX sales leader noted costly reliability problems with printheads: “Due to the learning curve, clients were doing things wrong and ruining their own printheads. This was a big problem for the clients and MTEX, and we were losing money. As a result, the printheads required a lot of maintenance.” [17]

Afinia was “engaged with MTEX and showcased their printing system two years ago at Label Expo. We had been engaged with them to OEM the product and act as their sales arm.” Afinia spent over a year working with MTEX – including time on-site at their headquarters in Porto, Portugal. They found that MTEX was unfocused and lacked a robust quality/reliability culture, often failing to finish the critical “last 10%” of development. The Afinia executive describes MTEX’s culture as “freewheeling,” explaining: “it wasn’t like a public company with established policies and procedures… the structure was lacking… during the engagement, it was clear that they weren’t used to our way of working.” Ultimately, Afinia walked away from the partnership because “we were not comfortable putting our name on it. Afinia is a well-recognized name in the industry for our products, quality, service, and the support… we won’t be pressured into things that aren’t right for us to endorse.” [18]

In May 2024, AstroNova purchased MTEX in a transaction valued at over $20 million, despite the organizational immaturity and product reliability issues that are apparently well-known in the industry by this time. In a subsequent 1×1 call, CEO Greg Woods admits to us that AstroNova’s due diligence process was accelerated due to the timing of trade show Drupa and the believed presence of a competing bidder for MTEX. [19]

As subsequently communicated to investors, AstroNova’s rationale for buying MTEX appears to be supplier diversification – particularly away from Memjet. However, less than two years prior to the MTEX acquisition, AstroNova acquired Chicago-based Astro Machine, which was a Memjet OEM[20] that an SVP from Memjet described as a “very large Memjet customer… Memjet was the predominant product that they had.”[21]

According to an MTEX sales leader reporting directly to MTEX CEO Eloi Ferreira, AstroNova lacked an integration plan to address cultural challenges; AstroNova also did not seem to form relationships with MTEX employees; instead operating entirely through Mr. Ferreira – who is now involved in arbitration with AstroNova.[22] “ The American way of working-fast-paced and organized-wasn’t aligned with MTEX workflow and culture. The team wasn’t prepared for the challenge […] I didn’t have much opportunity to spend time with AstroNova’s leadership. Honestly, I only saw them a couple of times and exchanged a few words […] The relationship with AstroNova was entirely through Eloi. […] I don’t think [AstroNova leaders] were aware of the labor culture in Portugal, especially in the north. From my perspective, they didn’t care.”[23]

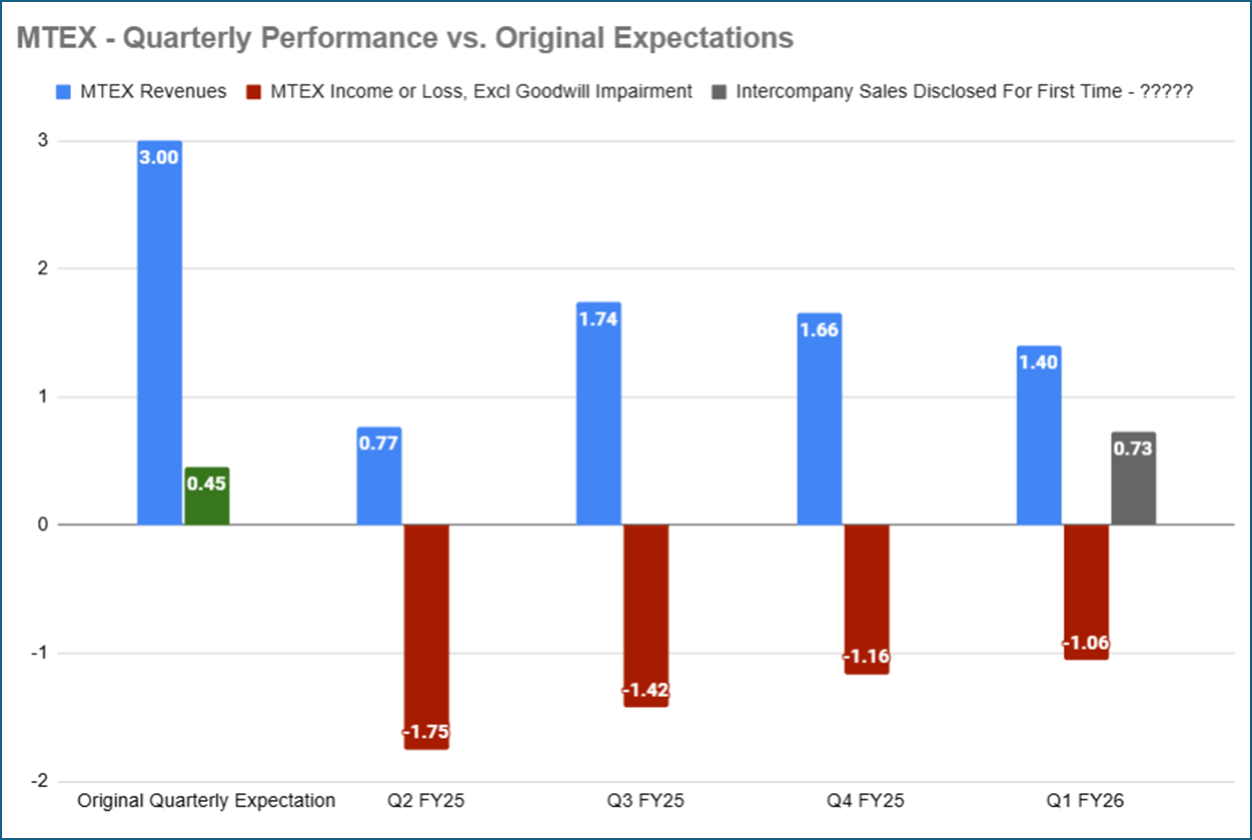

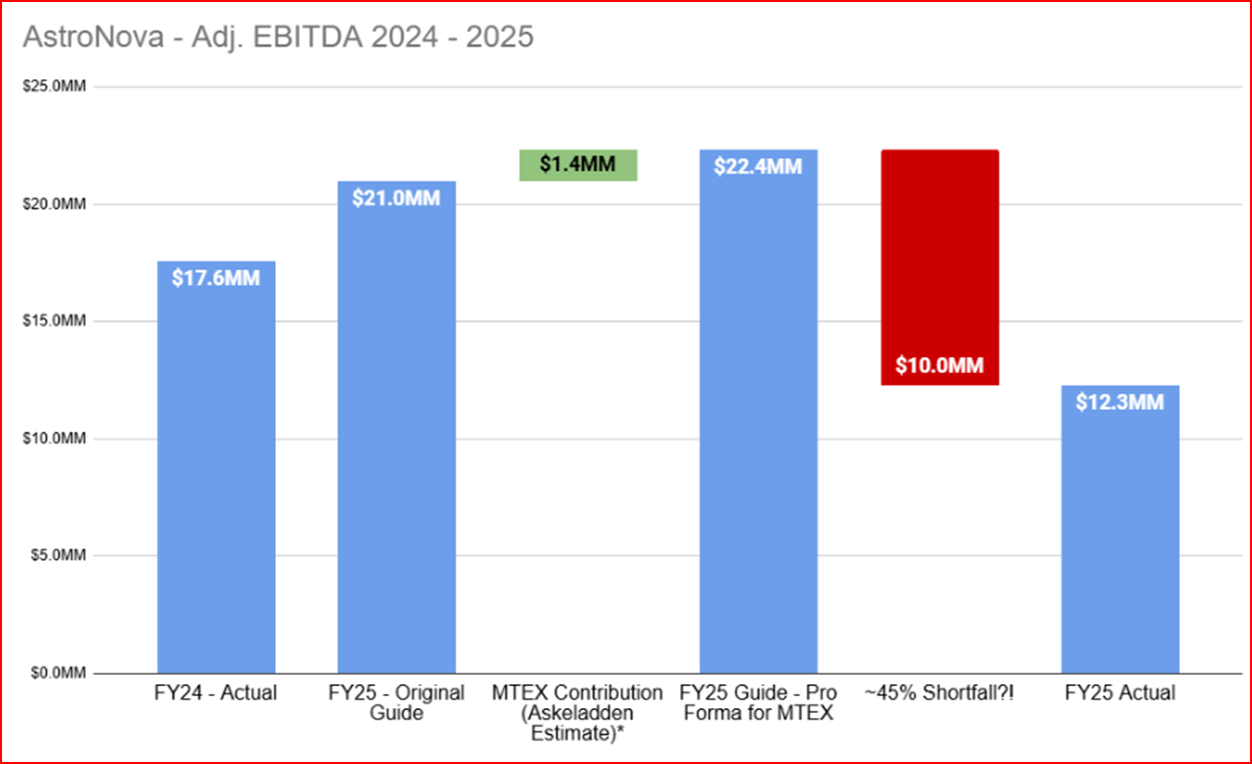

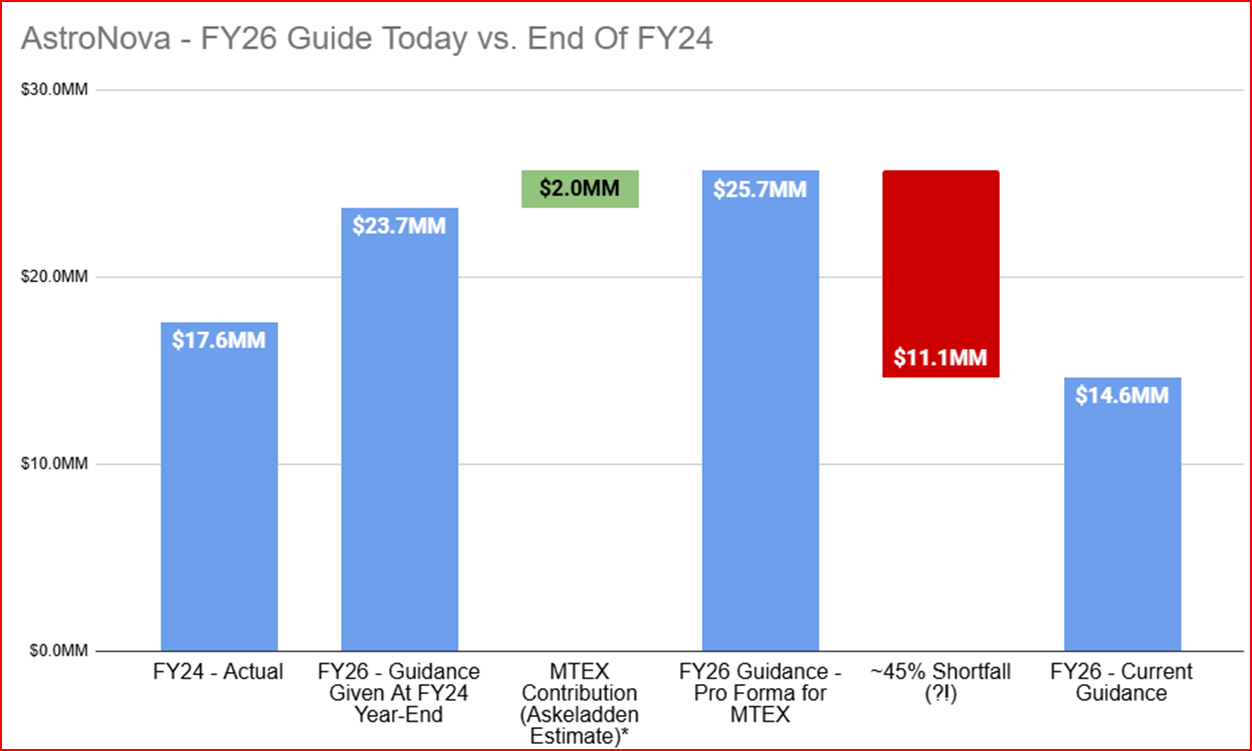

AstroNova initially expected MTEX to contribute $8 – $10 million in revenue for the balance of FY25 with significant growth thereafter and “ handsome” margins.[24] Despite CEO Greg Woods stating in September 2024 that MTEX had built a “strong backlog […] which will enable [MTEX] to meet our targeted revenue contribution,”[25] MTEX generated less than $4.2 million in revenues and $4.3 million in loss before tax for the full year, excluding goodwill impairment.[26]

At the end of FY25 (less than one year after the acquisition), AstroNova records a $13.4 million impairment , representing 70% of the cash outlay for MTEX, and discontinues 70% of MTEX’s product portfolio , which it refers to as “low-profit.” [27]

As a result of ongoing losses at MTEX and the debt used to fund the acquisition, AstroNova breaches its debt covenants and thus suffers an event of default on its credit facility (thus forcing AstroNova to seek a waiver and deferred repayment schedule from its lender, which was subsequently granted).[28]

In the recently-reported Q1 FY26, MTEX revenues decline sequentially from $1.66 million to $1.4 million; MTEX loses roughly $1 million in earnings before taxes. For the first time, AstroNova provides a confusing and poorly-explained disclosure which attribute roughly half of MTEX’s revenues to “intercompany sales” and refer to MTEX as a cost center rather than a standalone business.

Despite the apparent lack of commercial momentum related to existing MTEX products, CEO Greg Woods continues to refer to products based on MTEX technology as “highly disruptive.”[29] If MTEX technology is so disruptive… why is nobody buying it?

AstroNova has released several new products based on MTEX technology, and plans to release numerous additional products over the balance of the fiscal year. [30]

AstroNova continues to tout its “opportunity to improve margins […] through our multi-source ink supply program based on our new print engine technology.”[31] However, the Afinia executive further explained that the multi-sourced ink approach could lead to printhead damage and render customer machines unreliable or unusable until AstroNova fixes them. [32]

We believe this series of unfortunate events highlights a comprehensive failure of corporate governance on the part of AstroNova’s Board (including Mr. Woods, who serves as both CEO and Board member.) Specifically:

Governance Failure 1: Lack of Coherent Long-Term Strategic Planning. We believe the MTEX acquisition should be evaluated in context of AstroNova’s previous acquisition – Astro Machine. It is strategically incoherent – and fiscally irresponsible – to spend $17 million of shareholder capital in 2022 to purchase a company heavily reliant on Memjet, then to spend over $20 million of shareholder capital in 2024 to diversify away from the same reliance that was just increased.

Governance Failure 2: Approving MTEX Acquisition Despite Accelerated Due Diligence. Mr. Woods has admitted that due diligence was accelerated.[33] At the time of the acquisition, the company touted “handsome margins” and made no indication that 70% of the company’s product portfolio was low-profit. The company’s initial expectations for MTEX’s revenue and profitability seem clearly unrealistic.

Governance Failure 3: Lack Of Evaluation Of Alternatives.

As we discussed extensively in our primary research analysis , and expound upon later with Afinia’s experience, AstroNova had other options to diversify its supplier base; the Afinia executive stated he did not believe AstroNova would have needed to spend $20 million to develop and launch products akin to those that it is launching today. Instead, it rushed into the MTEX acquisition.

Governance Failure 4: Lack of Integration Plan and Contingency Plan for Key-Man Risk.

AstroNova appeared to have limited to no understanding of the challenges it would face in incorporating a “ freewheeling “entrepreneurial company lacking “established policies and procedures”[34] into the internal-controls environment of a publicly-traded company. AstroNova “didn’t care”[35] about the differences between Portuguese and American culture. AstroNova lacked an integration plan, failing to build relationships between AstroNova leadership and MTEX employees, instead relying entirely on its relationship with MTEX CEO Eloi Ferreira – which soured to the point that Mr. Ferreira and AstroNova are now engaged in legal proceedings.

Compounding the overly optimistic expectations for MTEX profitability based on limited due diligence, the quantum of debt used to finance the acquisition has put the balance sheet at risk. Shareholders were told in June 2024 that “we have the goal of repaying most […] of the revolving credit debt by the end of the year.”[36] Instead, the company breached its covenants, suffered an event of default, and was forced to seek extended repayment terms from its lender. If the lender had not waived the event of default or agreed to a deferred repayment schedule, AstroNova could potentially have been forced to seek rescue financing on unfavorable terms.

Governance Failure 6: Doubling Down Rather Than Reevaluating.

AstroNova appears to be stuck in the sunk-cost fallacy. The company cannot recover the cash lost as a result of overpaying for an immature company, but it can avoid doubling down on a bad hand. Unfortunately, as we will discuss later, rather than admitting that the MTEX acquisition was a mistake, the company appears to be taking a “bet-the-farm” approach and rapidly rolling out numerous new products, several in market segments that are new to the company, on the basis of MTEX’s technology. The company appears to be careening from an unwise overreliance on Memjet to an unwise overreliance on MTEX technology, rather than establishing a truly diversified technology base.

As discussed, this technology has historically experienced reliability issues, may have intrinsic flaws due to the provenance of its development, faces apparent competition from the Chinese supplier UPG with whom the technology was co-developed, and which has yet to demonstrate any sort of commercialization maturity or product-market fit, given the tepid and sequentially declining MTEX revenues reported by AstroNova from Q3 FY25 – Q1 FY26.

Conclusion

The governance failures we identify are not isolated incidents – they reflect a consistent pattern of poor judgment, inadequate oversight, and a Board that has lost its strategic compass. If elected, Askeladden nominees would correct these governance failures by immediately creating a new Strategy and Risk Committee , whose primary near-term objectives would be a comprehensive re-evaluation of the product portfolio, ensuring that AstroNova’s brand and reputation are not further damaged by rushing immature products to market. A longer-term objective will be thoughtful diversification of underlying print-engine and technology platforms. Such an endeavor, as we discuss in the next section, is something that smaller competitor Afinia has accomplished – it remains puzzling why AstroNova is either unable or unwilling to appropriately diversify.

Section 2: Detailed Analysis of Key MTEX Challenges

AstroNova’s governance failures are now operational risks. Below, we present detailed analysis of several key MTEX challenges that we believe AstroNova’s Board failed to recognize and appropriately respond to.

2.1: Ongoing Competition from UPG

While AstroNova presents MTEX’s technology as disruptive and proprietary, we believe that it in fact faces like-for-like competition from the Chinese supplier (UPG) with whom it was co-developed. The Afinia executive noted that “ UPG Group has shown these systems at trade shows, ” and UPG’s website indeed has a press release announcing their participation at Drupa in 2024[37], where AstroNova and MTEX also presented. The executive expressed concern that AstroNova’s sales may be hampered by ongoing competition from UPG:

“I think the big thing is to look at their relationship and how things go with the UPG Group. It makes the situation a bit difficult for other people to engage with AstroNova because since it’s been at the exhibitions and shows, their product, from what we have out in the market and the quotes they’re giving out, is going to be cheaper, of course, on hardware and probably cheaper ink. So, I don’t know how those two are going to play together in this industry between AstroNova and UPG Group. I don’t know what’s in their contract, but it’s going to make people leery about selling it, especially through a channel when they know the Chinese can come in and probably sell it for five grand less.”[38]

We have not yet comprehensively compared products marketed by UPG to products marketed by AstroNova. However, we have identified at least one stark example. UPG’s “LQ-MD M330 Label Printer”[39] appears nearly identical to AstroNova’s recently-launched QL-425 and QL-435 printers (which we believe are substantially similar to each other than their media width).

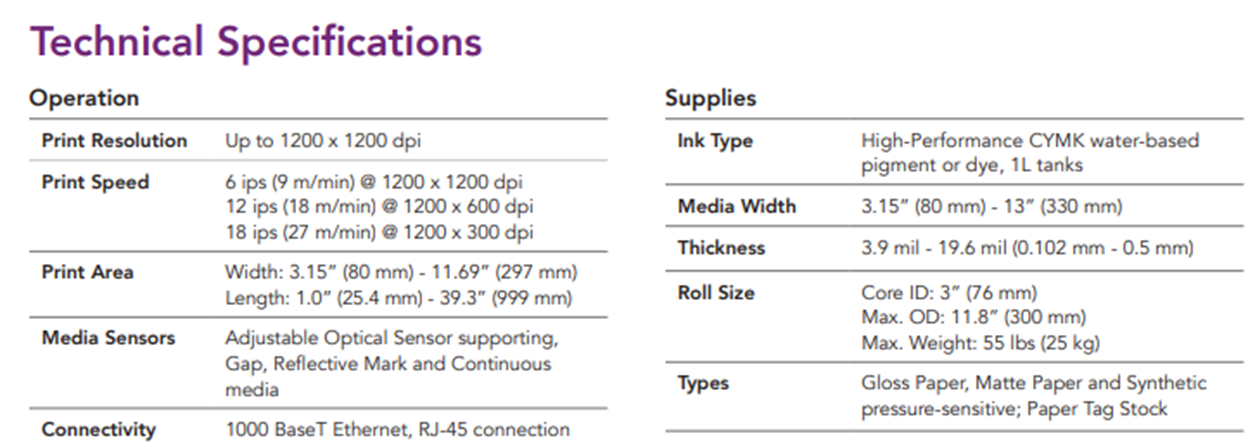

UPG and AstroNova’s products bear a striking visual similarity. Moreover, the products’ technical brochures also display substantially similar specifications. For example, as shown in the image below, AstroNova’s QL-435 brochure[40] references a 1-liter ink tank holding water-based CMYK pigment or dye inks, maximum of 1200 x 1200 dpi, a print speed of 18m/min at 1200×600 DPI, a maximum media thickness of 0.5mm, and a maximum print width of 297mm.

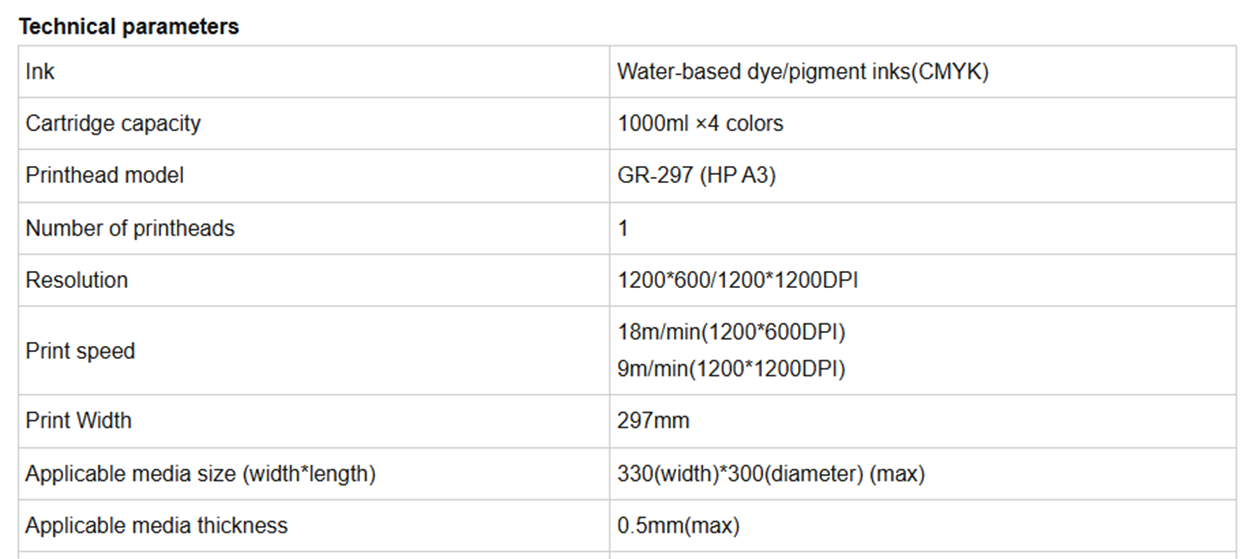

Meanwhile, as shown in the image below, technical specifications on UPG’s website for the LQ-MD M330[41] match all of these criteria:

Key governance failure: AstroNova’s Board either failed to realize that MTEX’s development partner was planning to compete with its products in the marketplace – or worse, realized it, yet proceeded to pay a high price for MTEX anyway.

2.2: Reliability and Quality Challenges Potentially Inherent To MTEX Technology

We believe that AstroNova’s decision to bet much of its future on MTEX technology – a platform with known reliability issues, potentially caused by its co-development with a Chinese supplier – is not just a failure of governance; it is arguably a more reckless and costly mistake than the company’s prior overdependence on Memjet.

As referenced in our primary research analysis , we twice interviewed a senior vice president from Memjet who cited reliability issues with MTEX products.[42] A former MTEX sales leader reporting directly to MTEX CEO Eloi Ferreira corroborated some of these challenges:

“Due to the learning curve, clients were doing things wrong and ruining their own printheads. This was a big problem for the clients and MTEX, and we were losing money. As a result, the printheads required a lot of maintenance.” [43]

Meanwhile, a former Sales Director at AstroNova said he did not perceive the MTEX technology as “ specifically good ” and called it “ basically very cheap. It’s more of a desktop-style printhead from HP.”[44]

Meanwhile, the Afinia executive explained that after over a year, Afinia ultimately walked away because it was not comfortable associating its brand with MTEX:

“We were not comfortable putting our name on it. Afinia is a well-recognized name in the industry for our products, quality, service, and the support we provide both pre-sales and post-sales. After a year and a half, or whenever this whole thing started, we [we]re not at the comfort level needed to ensure its viability in the market and its true commercialization.”[45]

Afinia wouldn’t risk its brand on even one MTEX product. AstroNova bought the whole company – and is now building much of its future on the same technology platform Afinia walked away from.

The Afinia executive went into far more depth on the quality and reliability challenges associated with MTEX technology’s original provenance:

“This project involved acquiring an engine from the open market. I can’t say whether it was bought through repair shops or spare heads […] this engine, we all know, is an HP engine. This was taken off the open market and developed without interaction from the manufacturer […] There are all kinds of things out there, including refurbished parts. If you go to an HP partner and say, “Hey, I need 10 or 20 heads,” I don’t know if they ask many questions, especially in places like China. They just care about revenue, so they keep selling you print heads. […]

When you do that, you won’t be able to call Epson or HP and say, “Hey, how do I write the driver for this?” or “The software isn’t interacting with the print head properly,” or “The timing isn’t right,” or “It’s not feeding at the correct rate.” You have to build all this stuff, and not being an expert or the one who built the print head, it gets quite complicated. Your end product may not optimize that engine because you don’t know all the inner workings. You might get it to work and it could be okay or good enough, but you don’t get that expertise from the manufacturer. […]

We’ve all had printers where the ink clogs, and you see lines or other issues. I’m guessing they’re probably discussing not having the specifications for these maintenance modules and how to keep the print head healthy. What is the schedule? It’s complicated to keep these print heads alive and functioning optimally. Without the specifications, knowing how often to perform maintenance, or understanding the capping pressure, it’s challenging. […] There’s a whole sequence, and it’s complicated. Without proper training, if people insert materials that are too thick or don’t stay within tolerances, the material can crash into the head. I’m guessing that was happening too. When you crash the head, it’s done. If something crashes into the head, you have to replace it.”[46]

It is possible that AstroNova may now be sourcing printheads directly from HP. If so, we invite the company to clarify this – shareholders deserve transparency about the technology the CEO repeatedly describes as “disruptive.”

Governance failure: AstroNova is basing a substantial portion of its future product portfolio on a technology platform that may be fundamentally unreliable. We do not know if AstroNova has re-engineered the MTEX platform in collaboration with HP to address the serious deficiencies cited above. But if the company is now working directly with HP, it raises yet another critical governance question: why did the Board approve a $20 million acquisition of MTEX – an immature company working with a Chinese supplier (and apparently now competitor) seemingly using components sourced on the open market – instead of partnering with HP from the outset?

If AstroNova ultimately arrived at a relationship directly with HP, then the entire MTEX detour through Portugal and China was a costly, unnecessary, and avoidable mistake. One that shareholders paid for.

Subsequent to the MTEX acquisition, we were initially excited about AstroNova’s promises regarding “multi-sourced inks.” In light of new information, we have serious reservations. Recall the printhead maintenance issues cited by the former MTEX employee. The Afinia executive pointed to a likely cause: multi-sourced inks can interact unpredictably with printheads – and with each other – increasing the risk of damage and system failure.

“Epson, Canon, and HP optimize their inks for these print engines. If they say a print head is good for 20 liters of ink, they’re usually conservative, knowing the ink won’t burn out the print head until after 20 liters. In this scenario, when you source your own ink, you need to do extensive testing to ensure it doesn’t damage the print head. […] If you don’t have a single source or have multiple sources, you need to understand what happens when those inks mix in the delivery system. There are still inks in the tubes and in the print head. If you get two different inks in there, how do they react? Do they lessen the life of the print head or burn it out? There’s a risk involved. If it says 20 liters, you have to test your ink. Companies like HP and Epson test for years and spend millions of dollars. It’s up to the individual to decide how much testing to do. They might just say it’s good enough and choose an ink to buy.”[47]

As we will discuss in Section 3, it took AstroNova over two years to resolve a quality issue tied to a single supplier – Memjet. Afinia fixed the same problem in six months.

What happens if AstroNova now introduces multiple ink suppliers? Any cost savings could be quickly erased by a new wave of quality failures.

The Afinia executive also noted that this platform is more complex than the Trojan T2-C – one of the printers affected by AstroNova’s unresolved ink issues. [48]

“The print head on [the Trojan T2-C] is much less complicated than an HP that’s been taken off the market. To replace a print head, you click in the software, it uncaps a little lid, you pull it out, similar to how you replace a print cartridge at home. You pop a new one in, close the cap, and it goes through its maintenance and service. With these machines, you’re talking about removing screws and unbolting components. Once you install the new print head, you have to go through an alignment process to align all the jets. It’s complicated. It’s not something someone making labels for jams and jellies can do without training. […] Those who buy this equipment expect it to run 24/7. If it doesn’t, someone from AstroNova will need to get on a plane or in a car to go there and fix it.” [49]

Governance failure: Management is now layering added complexity onto an already fragile platform, in pursuit of cost savings that could be easily undone by reliability problems, despite the company’s own history of quality failures, including a two-year struggle to resolve a single-supplier ink issue. We believe shareholders deserve substantial transparency into the quality and reliability testing that has been performed on the many new products that AstroNova aims to launch in quick succession on the basis of MTEX’s technology platform.

2.4: MTEX’s Organizational Immaturity

After more than a year working with MTEX, the Afinia executive offered blunt criticism of its maturity and execution, noting that “everybody in the industry” knew their Atom 1 [50] product “didn’t work.”

“It wasn’t like a public company with established policies and procedures. It was more of a freewheeling environment where you experiment and come up with different things. The structure was lacking, which is not typically how we operate. With the right partner, we weren’t looking for 10 products; we focused on one. During the engagement, it was clear they weren’t used to our way of working. There was a lack of focus, trying to do too much at once. It was spread so thin that anyone can get a printer to 90%, but that last 10% to make it a sellable product is tough.

When you have a bunch of products at 80%, you have nothing. You have to push them across the finish line, which sometimes requires hard work and hearing things people don’t want to hear. Looking back, and this is public knowledge, they did the Memjet project several years ago, which turned out to be a disaster. They didn’t finish their product. There are great Memjet products in the marketplace, but they couldn’t take theirs across the finish line. Everyone in the industry knew it didn’t work.”

Samir Patel: “You’re still talking about MTEX?”

Afinia Executive: “Yes, when they had the Memjet. I think it was called the Atom 1.” [51]

Governance failure: The Board appears to have overlooked, ignored, or failed to investigate MTEX’s lack of institutional maturity, quality controls, and product discipline – all of which were apparently well-known in the industry.

Section 3: Further Analysis of Other AstroNova Challenges

3.1: AstroNova’s Perplexing Struggle To Diversify Away from Memjet

In our primary research analysis , we extensively discussed AstroNova’s over-concentration with printhead supplier Memjet. The Afinia executive expressed confusion about AstroNova’s difficulties in organically developing alternatives to Memjet technology, something Afinia – even as a smaller company – managed to accomplish:

Afinia Executive: “We just deal with [Memjet]. We can’t change their business model. It has to make sense for them, and then we decide if we continue doing business with them.”

Samir Patel: “To that point, AstroNova makes a big deal about not being able to move away from Memjet without acquiring MTEX. I would think there were other options, as Memjet is not the only supplier in the world.”

Afinia Executive: “That’s a true statement. You can move away. We have Memjet, HP, and OKI. We have toner-based equipment and UV equipment. There are many alternatives […] there are different technologies available.”

Samir Patel: “So you’re saying they didn’t have to buy MTEX? AstroNova did not have to buy MTEX to move away from Memjet technology if they really wanted to?”

Afinia Executive: “This is just my opinion. With the expertise inside AstroNova, between TrojanLabel, AstroNova, and the Canon systems they have, along with HP box printers through the channel, I don’t think it would take $20 million for them to build the system by themselves. Maybe they felt it was the fastest way to market, but I don’t think it would have taken $20 million to build the new [QL-]425 or [QL-]435. That’s my opinion. I don’t know who said that was the only way.”[52]

It’s competitively rational for Memjet to leverage its position; nonetheless, many companies, including Afinia, use Memjet successfully. The key is maintaining alternatives. With a balanced supplier strategy, Memjet can still be a valuable partner – just not the only one.

Who is to blame for AstroNova’s historical inability to organically diversify away from Memjet? According to this Afinia executive, the problem is certainly not with AstroNova’s “ incredible… rockstar ” Chief Technology Officer Mike Natalizia:

“Mike is incredible. He’s a good guy, and I have nothing negative to say about him. I talk to him all the time. He was given a very difficult situation that they’re working in now, and he’s been a rock star.” [53]

This mirrors comments made by others. One other relevant quote comes from a former manager at Epson, who rated AstroNova’s technical capabilities only a two or three out of five, but stated:

“Mike Natalizia is very knowledgeable and understands the technology well.” [54]

AstroNova purportedly bought MTEX for its technological expertise and product development, but industry veterans have observed that MTEX’s products were immature and had known reliability challenges. Moreover, MTEX has less than $6 million of reported revenue in the trailing four quarters. Conversely, AstroNova has spent $6.6, $6.9, and $6.8 million on product development in the past three years – more than MTEX’s entire revenue! [55]

If AstroNova has a sizable product development budget, and its Chief Technology Officer Mike Natalizia is well-regarded as “very knowledgeable” and an “incredible… rock star” by industry peers – then why could AstroNova not organically develop products based on alternative printheads, as MTEX and Afinia both did, despite far fewer resources? What is the “difficult situation” that Mr. Natalizia is trying to make the best of, according to the Afinia executive? We believe it could only come from one direction – the very top of the company.

Recall that we previously heard criticism of AstroNova’s “dinosaur” [56] trade-show dependent marketing strategy from industry peers, as well as former AstroNova employees such as a former sales manager. [57] A former Sales Director at AstroNova explained that the sales organization pleaded with CEO Greg Woods to allocate funds to a modern approach, but he appeared uninterested in others’ feedback:

Sales Director: “In a nutshell, it was not just me, it was also our VP [of] Sales saying exactly the same thing. He put quite some emphasis on getting batch budgets allocated to SEO, SEA [search engine advertising], and so on, but it was never really done in a consequent[ial] manner. At the end, it always was “Well, no, we had so much success in the past with the trade shows. Let’s do that right.” […] It really comes from the top of the company really, I have to say that. […]”

Samir Patel: “Just to clarify […] you’re saying Greg Woods wants to go to these trade shows regardless of what his VP of sales and the people who are actually selling and trying to generate leads are telling him […].”

Sales Director: “Exactly. I would certainly go that far.”[58]

Mr. Woods is apparently equally uninterested in participating in collegial industry discussions -the Afinia executive explains:

“All the other companies on the desktop were constantly, communicating. What are you seeing in the market? What are you doing about this? I don’t know if Greg doesn’t know about the industry, doesn’t care, or thinks he already knows what’s going on and doesn’t want to engage, but I can count on one hand the times we’ve probably even spoken […] I’m sure you know Primera, NeuraLabel. All of us, we always go at shows or talk a few times a year and want to compare notes. Not him. I don’t know if he reaches out to other people in the industry, but with us and our size and our volumes and what we do, you would imagine he would. But the only time we’ve ever reached out is if they wanted to buy us.”

Perhaps if Mr. Woods had spent more time engaging with industry peers, he would have learned about the various quality and reliability issues plaguing MTEX, or identified alternative options to develop innovative new products without spending over $20 million of shareholder capital on the poorly-conceived, poorly-diligenced, and poorly-planned MTEX acquisition.

Governance Failure: The Board failed to hold management accountable for developing internal alternatives to Memjet, despite ample resources, talent, and market options.

Askeladden Response: Developing a truly diversified technology base will be a critical priority for our newly-established Strategy and Risk Committee.

3.2: AstroNova’s Quality Culture

Recall that we spoke to a TrojanLabel customer who had faced numerous, “existential” quality issues with AstroNova media that had shut down his production for a week during peak season,[59] and a quality manager on the Aerospace side of the business who stated “ when it came down to making a shipment for revenue, that was priority and that was the culture… if it was functioning even marginally, it was a shipment, it was going.” [60]

The Afinia executive shed more light on Memjet-related quality issues. While these took AstroNova more than two years to fully resolve[61], Afinia fixed the same problem in six months due to its focus on quality and customer satisfaction:

“Regarding the ink on Memjet, yes, there was an issue with contamination and shelf life […] Our approach was to mitigate the damage in the marketplace. Whether it involved swapping out ink with new ink or disposing of some inventory, we tried to mitigate it on our side as much as possible. If AstroNova kept shipping the old stock and then switched to the new formulation, I’m not privy to that information. We took corrective action, and that’s the only way I can explain why they had so many problems.

[…] There were various things we ended up doing. Some of it involved absorbing some inventory costs and assisting customers if they had issues, as these were quite sporadic. Another thing we did was implement filtration systems to mitigate the problem. We provided accessories to customers that could be attached to the ink delivery system, which included a set of micro filters. It was fairly straightforward. And we resolved it.

[…] We just did what needed to be done. We’re the type of company that, because we’re not public, focuses on taking care of our customers. We took corrective actions, but it wasn’t a one-size-fits-all solution since every customer had different scenarios. Some received fresh ink immediately, others used filters, and sometimes we provided free ink or swapped out products or gave a free print head. We aimed to keep everyone satisfied, and I think we dealt with that for about six months.” [62]

Governance Failure : AstroNova’s Board tolerated a culture that prioritized shipments over quality and failed to instill the accountability needed to resolve customer-facing issues in a timely manner.

Askeladden Response: We believe quality cultures are instilled from the top of organizations. Our slate believes that maximizing the value of an installed base starts with treating customer satisfaction and product reliability as non-negotiable – not optional. Unlike the current Board, Askeladden’s slate will prioritize proactive service, rapid issue resolution, and quality-driven culture to protect the brand and unlock the full lifetime value of every customer relationship.

3.3: AstroNova’s Competition with its Own Channel Partners

Recall that we have previously heard many criticisms of AstroNova’s mismanagement of its channel partner relationships. A Senior Vice President at Memjet explained:

“They’ve struggled to really, even as a public company, with the resources they’ve got, outcompete on the channel marketing skills of somebody like an Afinia.”[63]

Others, such as a Managing Director at OKI, explained to us why especially in Europe, a channel approach is superior to a direct approach due to differences in local language and culture.[64] The OKI executive also commented on AstroNova’s bizarre approach of trying to partner with OKI to go to market, then undercutting OKI on price.[65]

The Afinia executive also described AstroNova poaching sales from its own dealers – a shortsighted tactic that sacrifices long-term channel trust for small, short-term gains, ultimately undermining future revenue growth.

“Yes, we are channel-based, and the reason for that is many of these systems require people who would like more local support. […]

[AstroNova] typically sell[s] direct. They say they have some partners, but typically the partners don’t sell a lot because we know them. They may show the product to get people to call them, but they won’t sell much. What ends up happening is they train the customer, do samples, and invest time and money.

Then, if the customer calls AstroNova or QuickLabel Systems directly, they’ll offer a discount, like selling it for two grand less. The dealer then calls the customer back, only to find out the customer bought directly from AstroNova at a better price. There’s a huge conflict. They’ve tried to have a channel before but have been unsuccessful because they have people selling direct.” [66]

Governance Failure: The Board has tolerated a go-to-market strategy that undermines long-term channel relationships in favor of short-term sales, impairing sustainable revenue growth.

Askeladden Response: We will prioritize implementing policies to prevent channel-partner conflict and hire a dedicated executive with demonstrated expertise in building and maintaining a successful channel strategy.

Section 4: Q1 FY26 Results Review

While we are more focused on longer-term strategic concerns at this point rather than quarterly results, we believe there are three elements of Q1 FY26 results that shareholders should carefully consider.

4.1: Inventory Balances

AstroNova has long promised to normalize elevated post-pandemic inventory levels, yet results continue to move in the wrong direction. For example, Mr. Woods promised in May 2023:

“We’re starting to work our inventory down… it’s definitely higher than what we need…. You’ll start to see that come down as we go through this year. We’ve got plans to do it. And we have good, reliable supply… we typically try to keep about three months’ supply.”[67]

On the Q4 FY25 earnings call in April 2025, Mr. Woods promised “decisive action”:

“we’re taking decisive action to reduce debt and improve cash flow through an inventory reduction program. These initiatives reflect our commitment to financial discipline and delivering value to our shareholders.”[68]

Decisive action on inventory balances remains nowhere to be found. We measure inventory balances by the “inventory days on hand” metric that AstroNova itself calculates and discloses in its SEC filings, which normalizes for the size of the business (given various acquisitions consummated over time). During Q1 FY26, inventory days on hand increased to 185, from 175 at year-end – exceeding the prior year-end peak of 176 (at the end of FY23).[69] By this metric, inventory balances are roughly 50% higher than levels in FY18 and FY19.

The company’s utter inability to reduce its inventory balances despite promises dating back years is directly harming shareholders. The company’s current inventory balances of $51.5 million exceed the company’s indebtedness[70] and represent more than 70% of the company’s current market capitalization – an incredible figure.[71] If the company converted its $15 – $20 million of excess inventory into cash, it would free up a substantial amount of capital to make organic investments and repay debt. (This is particularly critical given that merely a quarter ago, AstroNova breached its debt covenants, suffered an event of default, and was forced to seek a waiver and a deferred repayment schedule from its lender.) [72]

4.2: Lack of Self-Recognition and Accountability

Slide 4 of the company’s earnings presentation[73] includes a tone-deaf and accountability-free graphic including the words “value-generating M&A”:

The first step to self-improvement is admitting you have a problem. Highlighting “value-creating M&A” merely one quarter after a covenant breach and goodwill impairment related to the MTEX acquisition demonstrates an alarming lack of accountability. As referenced earlier, MTEX has not only failed to achieve original expectations, but its revenue has actually declined sequentially in Q4 FY25 and Q1 FY26. The company provides a poorly-explained disclosure attributing half of Q1’s $1.4 million in sales to “intercompany” sales[74], and MTEX continues to lose over $1 million per quarter.

The company’s own Form 10-K plainly states that MTEX’s current value, based on historical performance and future expectations, is dramatically below the original acquisition price:

Current year operating expenses included a $13.4 million goodwill impairment charge related to the under performance of the MTEX acquisition. Originally, we expected MTEX to achieve $8.0 million to $10.0 million in revenues for the period of May 2024 through January 2025, however, during this period, MTEX generated only $4.2 million of revenue. Due to the actual and expected underperformance of MTEX relative to our original expectations, we performed a strategic review of the MTEX operation, which ultimately led to the conclusion that the goodwill in our PI segment was impaired.

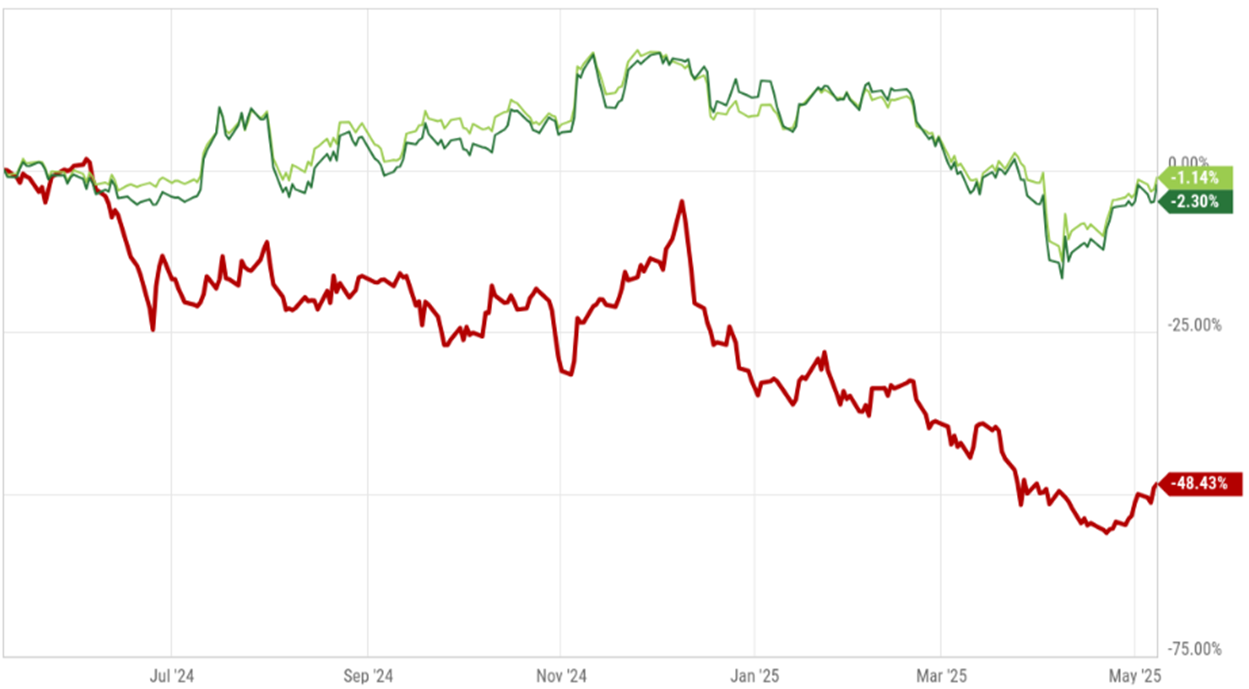

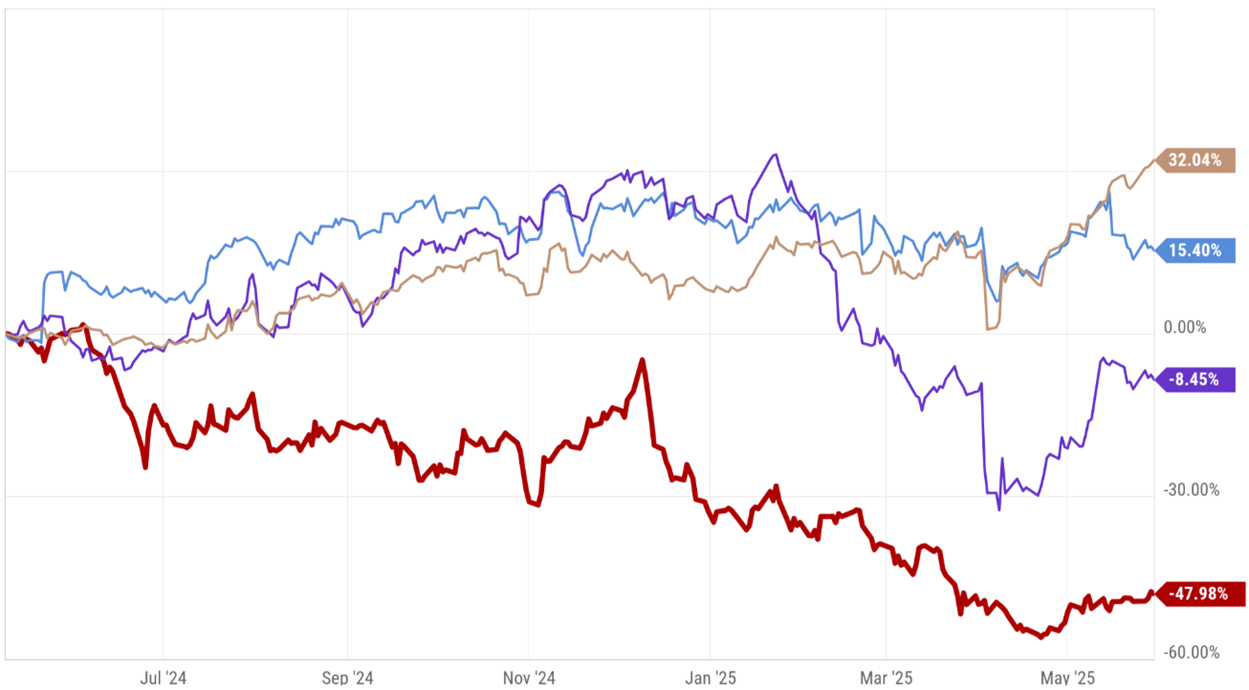

Over the year following the MTEX acquisition, AstroNova’s shares have also plummeted nearly 50%. During the same time period, small and micro-cap indexes had low single digit declines. Meanwhile, segment-specific benchmarks such as the iShares Aerospace ETF and industrial-printing peers such as Brady Corporation and Zebra Technologies had returns of negative 8% to positive 32%, as shown on the charts below based on data from YCharts.

Finally, the company’s Form 10-K also disclosed the termination of roughly 10% of the company’s global workforce in a restructuring action. So there is not a single framing we can identify in which it is whatsoever reasonable for management to make any claims about “value-creating M&A.”

4.3: Comparison to Q1 FY25 Results Without Acknowledging FY24 Results or Original Guidance

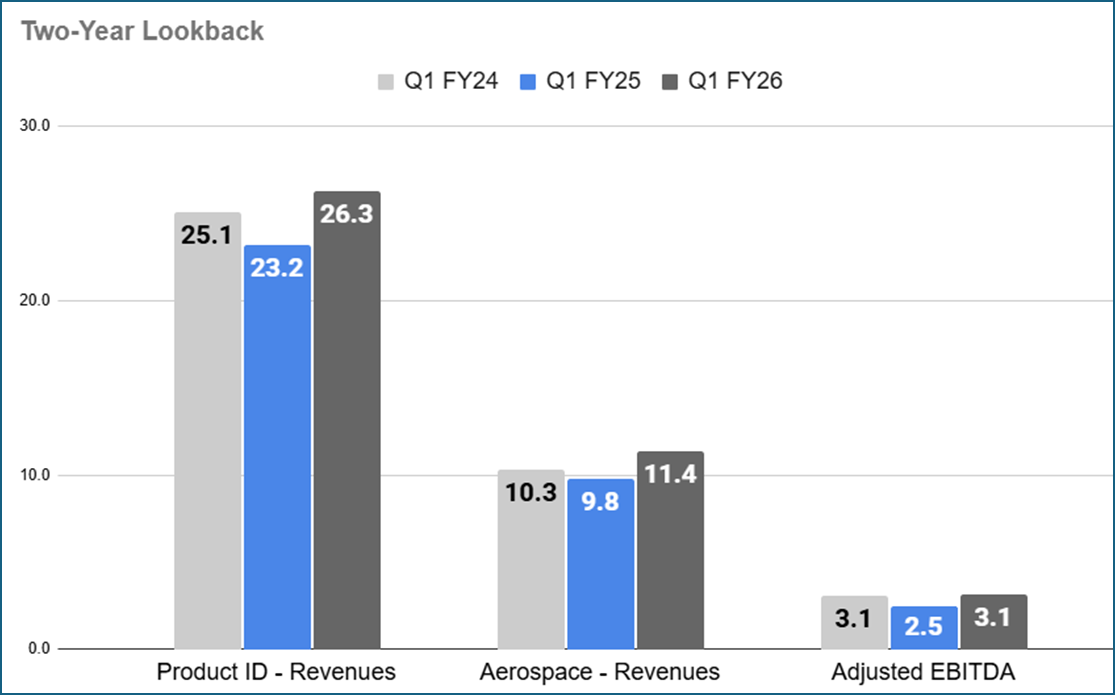

In the presentation and on the earnings call, CEO Greg Woods made much of the company’s double-digit year-on-year revenue growth in Q1 FY26. This certainly sounds impressive. However, a deeper look demonstrates that results continue to underwhelm.

First, we believe it is worth remembering that Q1 FY25 saw year-over-year declines in revenues in both segments. As such, a more accurate comparison is to revenues from two years ago. [75]

Further, there are important dynamics to note for each segment. First, in Product ID, the company’s own Q1 FY24 earnings release[76] notes that revenues were impacted by the then-ongoing ink quality issues that were not resolved until the end of FY24. So even Q1 FY24 results are not exactly a starting point to be excited about.

Second, we note that given the company’s dominant market share for ACARS printers in its Aerospace segment, revenue growth in the Aerospace segment is driven less by anything that AstroNova management is doing, but instead more by production rates at Airbus and Boeing, as well as delivering on shipments that were delayed last year. As Mr. Woods explained on the call in his own words:

“Backlog for the quarter declined by $2.8 million year-over-year to $25.5 million, primarily driven by clearing previously delayed shipments. As we move through fiscal 2026, we expect to benefit from our new product introductions and the increasing build rates with Airbus and Boeing.”[77]

Moreover, we believe that shareholders should be more focused on profitability metrics than revenue metrics; it is ultimately profitability and cash flow that drive shareholder value. While the company seems to be proud of its guidance for FY26, we note that expected results this year are well below actual results in FY24, and even farther below the company’s original guidance for FY25 and FY26 provided at the end of FY24. The subsequent acquisition of MTEX with over $20 million in shareholder capital should have improved upon earnings. The waterfall charts below demonstrate the significant shortfall relative to where earnings should be, according to AstroNova’s own words from 2024.[78]

Conclusion

We believe that AstroNova’s board violated their fiduciary duty to shareholders by consummating the MTEX acquisition. In review, MTEX:

Lacked institutionalized processes and procedures,

Operates in a new geography with a very different culture,

Operates in a new market segment with a very different customer base,

Co-developed its technology with a Chinese supplier who is now apparently selling similar products while undercutting AstroNova on price,

Has failed to achieve product-market fit with existing products, yet is being touted as the basis for many of AstroNova’s future products;

May face significant reliability and quality risks related to its products apparently being developed without OEM support and expertise in optimizing performance

Despite all of these challenges, AstroNova consummated the MTEX acquisition based on rushed due diligence, then failed to develop a credible integration plan. Is it any wonder that less than a year later, shareholders have suffered a nearly 70% impairment on the original cash outlay, lived through a covenant breach and event of default (subsequently waived), and suffered a nearly 50% decline in the stock price?

Even now, the Board is compounding past mistakes-doubling down on a failed strategy rather than acknowledging error and charting a better course. The Board is building a large portion of AstroNova’s future product portfolio on a technology platform with known reliability concerns -a decision that could prove catastrophic to AstroNova’s brand image given the company’s checkered past track record of resolving quality issues in a timely fashion.

Setting aside any other issues, we believe that the comprehensive failure of governance related to the MTEX acquisition represents a fireable offense. Indeed, we advocate that shareholders summarily dismiss Mr. Quain, Mr. Woods, Mr. Warzala, Ms. Schlaeppi, and Mr. Michas from Board service – instead electing Askeladden’s five nominees, Mr. Kravetz, Mr. Oviatt, Mr. Patel, Mr. Roberts, and Mr. Sands on the GOLD card.

I encourage all shareholders, large or small, to reach out to me directly if they wish to share their perspectives on AstroNova and discuss how our nominees can set the company on a path to a brighter future. I have committed to not accepting any cash or stock compensation for serving as a director (only customary reimbursement of expenses.) My sole motivation is the restoration of shareholder value on behalf of my clients and all long-suffering AstroNova shareholders.

I look forward to speaking with you individually and earning your vote. As a reminder, this Thursday, June 12 th , at 11 AM ET, we plan to host a virtual town hall meeting for AstroNova shareholders to interact directly with our nominees. You can register here .

Samir Patel, Askeladden Capital Management LLC, Jeff Sands, Shawn Kravetz, Ryan Oviatt and Boyd Roberts (collectively the “Participants”) filed a definitive proxy statement and accompanying proxy card with the SEC on May 20, 2025, as amended on May 21, 2025, to be used in soliciting proxies in connection with the 2025 annual meeting of shareholders (the “Annual Meeting”) of AstroNova, Inc. (the “Company”). All shareholders of the Company are advised to read the Proxy Statement and other documents related to the solicitation of proxies, each in connection with the Annual Meeting, by the Participants, as they contain important information, including additional information related to the Participants, including a description of their direct or indirect interests by security holdings or otherwise. The Proxy Statement and an accompanying GOLD proxy card will be furnished to some or all of the Company’s stockholders and is, along with other relevant documents, available at no charge on the SEC website at http://www.sec.gov , or by contacting Samir Patel at 1452 Hughes Road, Suite 200 #582, Grapevine, TX, 76051.

[1] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[2] “Former SVP at Memjet Believes AstroNova Needs Clear Marketing Strategy for Growth and Profitability.” Tegus. Published May 15, 2025.

[3] Tangentially, Afinia is also a customer of AstroNova; some of its products are produced by AstroNova’s Astro-Machine subsidiary.

[6] MTEX revenues disclosed in AstroNova’s filings as follows. Revenue of $768,000 and loss before taxes of $1.754M reported in Form 10-Q for Q2 FY25, filed September 17, 2024, see note 3 (10-Q does not appear to have page numbers.) Revenue of $1.74M and loss before taxes of $1.42M reported in Form 10-Q for Q3 FY25, filed December 12, 2024, see note 3 (10-Q does not appear to have page numbers.) Revenue of $4.163 million and operating loss of $16.88 million, including $13.4 million goodwill impairment, reported for full year on page 24 of the Form 10-K filed April 15, 2025. By subtraction, Q4 revenue is $1.657M. Q1 FY26 MTEX revenue of $1,402 reported on Page 10 of Form 10-Q for Q1 FY26, filed June 6, 2025, although for the first time, a disclosure reads that $727,000 of MTEX revenue was “related to sales that were sold to third parties via intercompany sales,” and also that “MTEX no longer operates as an independent business, but rather our manufacturing operation in Portugal is treated as a cost center. The majority of MTEX sales are through intercompany operations.” We do not have a clear interpretation of what this implies for like-to-like comparisons of MTEX’s revenue and cost structure to prior quarters where this disclosure was not made.

[13] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[14] Former [Sales] Director at AstroNova Believes Competitors’ Faster Solutions Pose Challenges and Emphasizes Need for Improved Online Presence. Tegus / Alphasense. Published May 7, 2025.

[15] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[16] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[18] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[19] We have signed affidavits from multiple other shareholders to whom Mr. Woods represented the same.

[20] Former Manager at Epson America Thinks AstroNova Must Embrace Advanced Technology to Compete With Chinese Rivals. Tegus / Alphasense. Published May 5, 2025.

[21] “Former SVP at Memjet Believes AstroNova Needs Clear Marketing Strategy for Growth and Profitability.” Tegus – May 15, 2025.

[22] Legal proceedings between Mr. Ferreira and AstroNova are discussed on page 19 of FY2025 Form 10-K, published April 15, 2025.

[24] MTEX Acquisition Announcement 8-K and MTEX Acquisition Call Transcript, May 9, 2024.

[25] AstroNova Q2 FY25 Earnings Call Transcript, September 16, 2024.

[26] AstroNova Form 10-K for FY2025.

[27] AstroNova Form 10-K for FY2025. Impairment discussed on page 11; purchase price discussed on page 15.

[28] Form 8-K filed March 21, 2025.

[29] Term “highly disruptive” used on both Q4 2025 Earnings Call Transcript – April 14, 2025 – and Q1 2026 Earnings Call Transcript – June 5, 2025.

[30] Q1 2026 Earnings Call Transcript – June 5, 2025.

[31] Q1 2026 Earnings Call Transcript – June 5, 2025.

[32] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[33] We have spoken with other shareholders to whom Mr. Woods has made similar statements.

[34] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[38] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[44] Former [Sales] Director at AstroNova Believes Competitors’ Faster Solutions Pose Challenges and Emphasizes Need for Improved Online Presence. Tegus / Alphasense. Published May 7, 2025.

[45] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[46] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[47] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[48] “Memjet Ink Issues.” Post by user “hgrunwell” on “Print Planet” forum on December 23, 2021. See also ensuing posts by users Ivilyn, schwarzmuller, and jwoyshnar discussing the same issues. https://printplanet.com/threads/memjet-ink-issues.291865/

[49] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[51] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[52] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[53] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[54] Former Manager at Epson America Thinks AstroNova Must Embrace Advanced Technology to Compete With Chinese Rivals. Tegus / Alphasense. Published May 5, 2025.

[55] FY2025 Form 10-K filed April 15, 2025. Page 22.

[58] Former [Sales] Director at AstroNova Believes Competitors’ Faster Solutions Pose Challenges and Emphasizes Need for Improved Online Presence. Tegus / Alphasense. Published May 7, 2025.

[60] “Former Quality Manager at AstroNova Believes Aggressive Change and Leadership are Key for Competitive Edge.” Tegus – Published May 6, 2025.

[61] FY2022 Form 10-K filed April 14, 2022 and Q4 FY 2022 earnings conference call transcript on April 14, 2022. FY2023 and FY2024 Form 10-K

[62] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[63] “Former SVP at Memjet Believes AstroNova Needs Clear Marketing Strategy for Growth and Profitability.” Tegus. Published May 15, 2025.

[66] Preliminary transcript of interview with C-level executive at Afinia, conducted via In Practise on June 5, 2025. Formatted transcript to be published in the In Practise database later this month.

[67] May 2023 Sidoti Micro-Cap Virtual Conference – Call Transcript.

[69] The inventory days on hand metric is referenced on page 31 of AstroNova’s Q1 FY26 Form-10Q, filed June 6, 2025. All data in the chart below is similarly sourced from the Form 10-K with the SEC for the relevant years.

[70] The company’s Form 10-Q, filed June 6, 2025, reflects $18.4 million outstanding on the line of credit, $6 million of current long-term debt, $327,000 of short-term debt, and $20 million of long-term debt, totaling just under $45 million – less than the company’s $51.5 million inventory balance. One could also consider the royalty obligations and lease obligations on the balance sheet as forms of indebtedness, but these would not change the math significantly.

[71] Data sourced from YCharts as of June 8, 2025.

[74] All data in the chart is sourced from AstroNova’s filings, other than the estimate of quarterly profitability, which is Askeladden analysis based on management’s discussion of “handsome” margins. MTEX revenues disclosed in AstroNova’s filings as follows. Revenue of $768,000 and loss before taxes of $1.754M reported in Form 10-Q for Q2 FY25, filed September 17, 2024, see note 3 (10-Q does not appear to have page numbers.) Revenue of $1.74M and loss before taxes of $1.42M reported in Form 10-Q for Q3 FY25, filed December 12, 2024, see note 3 (10-Q does not appear to have page numbers.) Revenue of $4.163 million and operating loss of $16.88 million, including $13.4 million goodwill impairment, reported for full year on page 24 of the Form 10-K filed April 15, 2025. By subtraction, Q4 revenue is $1.657M. Q1 FY26 MTEX revenue of $1,402 reported on Page 10 of Form 10-Q for Q1 FY26, filed June 6, 2025, although for the first time, a disclosure reads that $727,000 of MTEX revenue was “related to sales that were sold to third parties via intercompany sales,” and also that “MTEX no longer operates as an independent business, but rather our manufacturing operation in Portugal is treated as a cost center. The majority of MTEX sales are through intercompany operations.” We do not have a clear interpretation of what this implies for like-to-like comparisons of MTEX’s revenue and cost structure to prior quarters where this disclosure was not made.

[75] Data sourced from Form 10-Q for relevant years.

[77] AstroNova Q1 FY26 Earnings Call – June 6, 2025.

[78] AstroNova’s Q4 FY24 earnings release from March 22, 2024 explains: “For fiscal 2025, AstroNova expects to achieve full-year organic revenue percentage growth in the mid-single digits. Additionally, as AstroNova continues to drive operational improvements throughout the business, the Company expects its full-year adjusted EBITDA margin to be 13% to 14% this year and further improve by 100 basis points per year over the following two fiscal years.” 5% (mid single digit) growth would imply revenues increasing from $148.1 million to $155.5 million; the midpoint of margins (13.5%) implies $21 million based on that revenue. Similar math is used to arrive at our estimate for FY2026. MTEX estimates are based on management commentary at the time of acquisition, discussed extensively elsewhere in this document.

LAS VEGAS, NEVADA / ACCESS Newswire / June 10, 2025 / Avant Technologies Inc. (OTCQB:AVAI) (“Avant” or the “Company”), and its JV partner, Ainnova Tech, Inc., (Ainnova), a leading healthcare technology company focused on revolutionizing early disease detection using artificial intelligence (AI), today announced the Company is in the final stages of prototyping its proprietary automated retinal camera. Ainnova’s new device will offer users a low cost, easier to use camera that captures images automatically and then uploads those images to the Company’s Vision AI software platform, which then produces a “risk report” in mere seconds.

Vinicio Vargas, Chief Executive Officer at Ainnova and member of the Board of Directors of the joint venture company, Ai-nova Acquisition Corp., said, “The cost of a fundus camera has always been a barrier to entry into in this market, so our low-cost camera, which is a fraction of the cost of currently available cameras on the market, should allow us to not only enter the market, but to capture a large share of the market.

“Another significant advantage will be that our camera will be seamlessly packaged together with our Vision AI platform, allowing us to refer more patients in less time and accurately to medical specialists. Also, one of our objectives is to integrate other technologies to this preventive screening, expanding the scope from only diabetic patients to patients who have other risk factors and want to prevent other diseases from a more complete approach.”

Vision AI is a powerful cutting-edge, AI-driven platform that can quickly and accurately detect the early markers of a host of diseases by applying AI models to examine imaging data from the eye to expedite earlier detection and allow patients to better manage their disease. The diseases that Vision AI can detect, include diabetic retinopathy, other retinopathies, such as glaucoma, macular edema, age-related macular degeneration, and other anomalies, as well as other diseases that do not require retinal images, and instead, use other datapoints that Ainnova has integrated into the software like the detection of cardiovascular disease (CVD), type 2 diabetes, liver fibrosis, and chronic kidney disease (CKD).

Currently, Ainnova’s Vision AI software works well with any fundus camera on the market; however, Ainnova and Avant are aiming for exclusivity by developing a lower-cost, easier to use camera.

Ai-nova Acquisition Corp. (AAC), the company formed by the partnership between Avant and Ainnova, will develop the retinal cameras as part of the joint venture and licensing deal to facilitate the development of Ainnova’s technology portfolio. AAC owns the global licensing rights to develop, maintain, and market Ainnova’s technology portfolio.

About Ainnova Tech, Inc.

Ainnova is a Nevada-based healthtech startup with headquarters in San Jose, Costa Rica, and Houston, Texas. Founded by an experienced and innovative team that is dedicated to leveraging artificial intelligence for early disease detection. Recognized with multiple global awards and renowned partnerships with hospitals and medical device companies, we proudly introduce Vision AI – our cutting-edge platform designed to prevent blindness and detect the early onset of diabetes. Explore how Ainnova is revolutionizing healthcare through advanced technology and proactive solutions.

About Avant Technologies Inc.

Avant Technologies Inc. is an emerging technology company developing solutions in artificial intelligence in healthcare. With a focus on pushing the boundaries of what is possible in AI and machine learning, Avant serves a diverse range of industries, driving progress and efficiency through state-of-the-art technology.

Certain statements contained in this press release may constitute “forward-looking statements.” Forward-looking statements provide current expectations of future events based on certain assumptions and include any statement that does not directly relate to any historical or current fact. Actual results may differ materially from those indicated by such forward-looking statements because of various important factors as disclosed in our filings with the Securities and Exchange Commission located at their website (http://www.sec.gov). In addition to these factors, actual future performance, outcomes, and results may differ materially because of more general factors including (without limitation) general industry and market conditions and growth rates, economic conditions, governmental and public policy changes, the Company’s ability to raise capital on acceptable terms, if at all, the Company’s successful development of its products and the integration into its existing products and the commercial acceptance of the Company’s products. The forward-looking statements included in this press release represent the Company’s views as of the date of this press release and these views could change. However, while the Company may elect to update these forward-looking statements at some point in the future, the Company specifically disclaims any obligation to do so. These forward-looking statements should not be relied upon as representing the Company’s views as of any date after the date of the press release.

Owensville, OH – June 10, 2025 — HRT University has officially launched its signature HRT Master Course, a comprehensive, advanced training program designed to help licensed medical providers confidently and safely prescribe testosterone replacement therapy (TRT) and bioidentical hormone replacement therapy (BHRT). This new online course is tailored specifically for nurse practitioners, physician assistants, and physicians seeking to integrate hormone therapy into their clinical practice with greater precision and clinical depth.

The HRT Master Course was created by Nico Misleh, a board-certified nurse practitioner and the founder of HRT University. With years of hands-on clinical experience in hormone therapy, Misleh saw a critical need for a practical, no-fluff education that goes beyond theory and into the actual process of patient care. The course fills a growing gap in traditional medical training, where hormone optimization is often underrepresented or taught in overly complex or outdated ways.

“Providers know there’s growing interest in hormone therapy, especially TRT and BHRT,” said Misleh. “But many don’t feel adequately trained to implement it. This course gives them a complete clinical roadmap—based on real protocols and patient experience—not outdated textbooks or corporate models.”